This article is for informational purposes only and does not constitute financial advice. Consult a qualified financial advisor before making credit or financing decisions.

The best other apps like Klarna include Afterpay, Affirm, Sezzle, Zip, PayPal Pay Later, and Perpay. Each offers buy now, pay later financing with different approval requirements, spending limits, and fee structures. Shoppers with limited credit history tend to have the best luck with Perpay or Denefits, while Affirm and Splitit handle large purchases over $5,000.

Why People Switch from Klarna

Klarna works well for millions of users, but three specific limitations drive people to look for other apps like Klarna: low starting credit limits for new accounts, growing fee structures on monthly payment plans, and a merchant network that excludes many healthcare and service providers.

The app restricts spending limits for new accounts, sometimes starting as low as $100, and expands credit slowly based on repayment history. Users who need to finance a $600 appliance or a $1,200 dental procedure often hit a wall fast.

Late fees up to $7 per missed payment and Klarna’s recent move toward interest-bearing monthly payment plans have pushed cost-conscious shoppers to look elsewhere. Several competitors still offer genuine 0% interest with no fees at all, which Klarna once promoted as its core identity.

Afterpay is a buy now, pay later provider founded in 2014 that splits purchases into four interest-free installments over six weeks, with no fees unless a payment is missed. Affirm is a US-based BNPL lender founded in 2012 that offers 3-to-60-month installment plans with APR rates ranging from 0% to 36% and no late fees on any plan.

Merchant coverage is the other sticking point. Klarna integrates with roughly 500,000 retail partners globally, but that list skews heavily toward fashion and electronics retailers. Healthcare providers, auto parts shops, and service businesses often aren’t on it.

Top 12 Klarna Alternatives: Quick Comparison

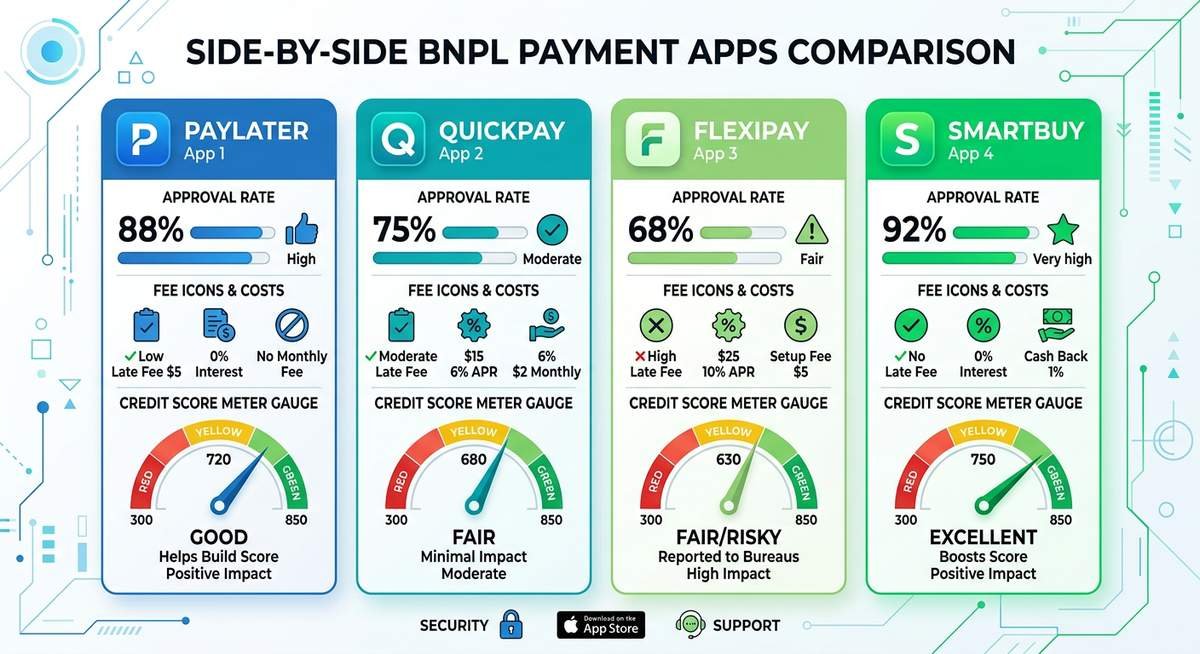

Afterpay, Affirm, and Sezzle consistently rank as the strongest general-purpose replacements, though each serves a different type of buyer. The table below covers the apps most worth considering, based on approval accessibility, fee transparency, and merchant network reach.

| App | Payment Structure | Max Financing | Credit Check | Late Fee | Best For |

|---|---|---|---|---|---|

| Afterpay | 4 payments / 6 weeks | Up to $2,000 | Soft | $8 or 25% of order | Fashion, beauty |

| Affirm | 3–60 monthly payments | Up to $25,000 | Soft | None | Large purchases |

| Sezzle | 4 payments / 6 weeks | Up to $2,500 | Soft | $10 / payment | Flexible rescheduling |

| Zip (Quadpay) | 4 payments / 6 weeks | Up to $1,500 | Soft | $5–$7 / payment | Anywhere Visa is accepted |

| PayPal Pay Later | 4 payments / 6 weeks or 6–24 months | Up to $10,000 | Soft | None | PayPal-friendly stores |

| Perpay | Weekly installments | $500–$2,500 | None | None | Bad credit / no credit |

| Sezzle Up | 4 payments / 6 weeks | Up to $2,500 | Soft | $10 / payment | Credit-building |

| Splitit | 2–24 monthly installments | Up to credit limit | None (uses existing card) | None | Large purchases, no new debt |

| CareCredit | 6–60 months | Up to $25,000 | Hard | Deferred interest | Healthcare, dental, vet |

| Cherry | 3–60 months | Up to $25,000 | Soft | Varies | Medical & cosmetic procedures |

| Denefits | 3–60 months | Up to $50,000 | None | None | Healthcare, 95% approval rate |

| Sunbit | 3–72 months | Up to $20,000 | Soft | Varies | Auto service, dental, optical |

Best BNPL Apps for Bad Credit and No Credit Check

Perpay approves over 90% of applicants regardless of credit score by tying repayments directly to your paycheck, making it the most accessible BNPL option for buyers with poor or nonexistent credit history.

Perpay operates as a closed marketplace, meaning you can only shop brands carried on its platform. That narrows the selection compared to open-network apps, but the tradeoff is a genuine no-hard-inquiry application and automatic paycheck deductions that eliminate late fees entirely.

Denefits reports a 95% approval rate, primarily serving healthcare providers who want to offer patients a payment option after insurance coverage runs out. If your provider uses Denefits, you can finance medical bills without a credit check and without interest.

Zip works at any merchant that accepts Visa through its virtual card feature, and like Perpay, uses only a soft credit pull. First-time limits start lower, around $200, but increase with on-time payments. For shoppers rebuilding credit, Sezzle Up reports payments to credit bureaus for a monthly fee, making it one of the only BNPL apps that actively helps raise your score.

The distinction between soft and hard credit inquiries matters more than most people realize. According to the Consumer Financial Protection Bureau, a hard inquiry can lower your credit score by up to five points and stays on your report for two years, while a soft inquiry has zero impact. Eight of the twelve apps above rely exclusively on soft checks.

Afterpay vs Klarna vs Affirm: Detailed Comparison

Affirm is the strongest choice for purchases over $500, Afterpay wins on simplicity for everyday retail spending, and Klarna sits in the middle without excelling at either end.

| Feature | Afterpay | Klarna | Affirm |

|---|---|---|---|

| Payment terms | 4 payments / 6 weeks | 4 payments / monthly / 1-shot | 3–60 monthly payments |

| Max limit (established users) | $2,000 | $10,000+ | $25,000 |

| Interest rate | 0% | 0%–24.99% APR | 0%–36% APR |

| Late fees | $8 or 25% of order | Up to $7 | None |

| Credit check type | Soft | Soft | Soft |

| Reports to credit bureaus | No | No (some plans do) | Yes (monthly plans) |

| Merchant network | 100,000+ in US | 500,000+ globally | 235,000+ in US |

| Virtual card (anywhere) | Yes | Yes | Yes (limited) |

Affirm’s zero-late-fee policy is a meaningful advantage for shoppers who sometimes miss due dates. Missing an Afterpay payment triggers an $8 fee and a temporary account freeze until you catch up, which compounds the frustration when you’re trying to use the app again.

Klarna’s monthly payment option looks attractive until you read the fine print: APRs on those plans can reach 24.99%, which is competitive with some credit cards and far from the interest-free positioning the brand built its name on.

Best BNPL Apps for Large Purchases

Affirm, Splitit, CareCredit, and Denefits are the only BNPL apps that reliably support purchases above $5,000, with Affirm and CareCredit offering up to $25,000 through formal monthly installment plans.

Splitit takes a different approach than every other app on this list. Instead of issuing you new credit, it splits an existing credit card purchase into installments with no interest and no fees, since the interest you’d pay (or not pay) is governed by your existing card’s terms. The ceiling is essentially your available credit limit, which for many cardholders is $10,000 or higher.

Affirm’s longer-term plans (up to 60 months) allow monthly payments on major appliances, home improvement projects, and travel bookings. The 0% APR option is available through select partner merchants, including Best Buy and Peloton. Off-merchant purchases through Affirm’s virtual card still carry interest, with rates that depend on your credit profile.

CareCredit’s 24-month and 60-month plans work similarly, with promotional 0% APR periods that convert to deferred interest if the balance isn’t paid in full before the promotional period ends. That deferred interest clause, buried in most users’ paperwork, catches many people off guard.

Does BNPL Affect Your Credit Score?

Most BNPL apps use soft credit checks that have no effect on your credit score, but Affirm’s monthly installment plans and CareCredit’s applications trigger hard inquiries that can lower your score by up to five points.

The credit score impact of buy now, pay later products has drawn increasing regulatory attention. According to a 2023 report from the Consumer Financial Protection Bureau, BNPL usage grew more than tenfold between 2019 and 2021, with five major lenders issuing 180 million loans worth $24.2 billion in 2021 alone. That growth has prompted ongoing questions about how BNPL debt is tracked and reported across credit bureaus.

Currently, Afterpay, Zip, and most 4-payment plans don’t report to credit bureaus at all, which means on-time payments don’t help your score either. Sezzle Up is the exception: subscribers pay a small monthly fee in exchange for payment reporting, functioning as a credit-builder product within a BNPL wrapper.

Late payments are a different story. Klarna, Afterpay, and Affirm can report delinquent accounts to collections after prolonged non-payment, which does impact your credit score significantly. The rule of thumb: BNPL is largely credit-score-neutral when used responsibly but carries real downside risk when payments are missed.

BNPL Fees Breakdown: What You’re Actually Paying

Affirm is the only major BNPL app with zero late fees across all plans. Most competitors charge between $5 and $15 per missed payment, and CareCredit’s deferred interest clause can result in retroactive interest charges of hundreds of dollars if you miss the promotional payoff window.

| App | Late Fee | Interest Rate | Account Fee | Rescheduling |

|---|---|---|---|---|

| Afterpay | $8 or 25% of order | 0% | None | 1 free / plan |

| Affirm | None | 0%–36% APR | None | N/A (fixed schedule) |

| Sezzle | $10 per missed | 0% | None | 1 free / plan |

| Zip | $5–$7 per installment | 0% | $1/order installment fee | Available (fee applies) |

| Klarna | Up to $7 | 0%–24.99% | None | Available in app |

| PayPal Pay Later | None | 0% (Pay in 4) / up to 29.99% (monthly) | None | Contact support |

| CareCredit | $28–$39 | 0% promotional / 26.99% deferred | None | No |

| Splitit | None | 0% (your card’s rate applies) | None | No |

Zip’s $1 per-transaction fee is easy to overlook in promotional material but adds up for frequent shoppers. Four purchases a month means an extra $4 in fees that never appear on the interest rate disclosures because they’re technically service charges, not finance charges.

The smarter question isn’t which app has the lowest fees, but which fee structure fits your payment behavior. If you sometimes need an extra week to make a payment, Sezzle’s single free rescheduling per plan is more valuable than Affirm’s no-late-fee guarantee on plans you’d always pay on time anyway.

Frequently Asked Questions

What is the best alternative to Klarna?

Afterpay is the best general-purpose choice among other apps like Klarna for retail shoppers. It offers 4 interest-free payments over six weeks, a 100,000-merchant network in the US, and straightforward terms without hidden fees. For large purchases, Affirm is the stronger choice due to its longer payment terms and zero late fees.

Which BNPL app has the highest approval rate?

Denefits reports a 95% approval rate, making it the most accessible option, though it primarily operates through healthcare providers. For general retail, Perpay approves over 90% of applicants by connecting repayments to your paycheck instead of your credit score. Zip and Sezzle also report high approval rates for applicants with limited credit history.

Do BNPL apps hurt your credit score?

Most BNPL apps use soft credit checks that have no impact on your credit score. Affirm’s monthly installment plans and CareCredit applications involve hard inquiries that may lower your score by up to five points. Missing payments can lead to collections referrals, which do cause significant score damage.

What is the difference between Afterpay and Klarna?

Afterpay only offers a single payment structure (4 payments over 6 weeks) with no interest, while Klarna offers multiple plans including pay-in-full, 4-payment, and monthly installments with interest. Afterpay has no APR products, making it simpler and lower-risk for everyday purchases. Klarna supports a much larger global merchant base.

Which BNPL app requires no credit check?

Perpay, Denefits, and Splitit require no credit check at all. Splitit works differently by splitting your existing credit card balance into installments, so no new credit application is needed. Perpay uses payroll data instead of credit scores to determine eligibility, bypassing credit checks entirely.

Can you use multiple BNPL apps at once?

Yes, you can use multiple BNPL apps simultaneously. There is no regulation preventing multiple active plans across different providers. However, managing several payment schedules increases the risk of missing a payment, and each new application may involve a soft credit pull that some lenders track when evaluating future applications.

Which BNPL app has the highest spending limit?

Denefits offers up to $50,000 in financing, making it the highest-limit BNPL option. Affirm and CareCredit both offer up to $25,000. Splitit has no fixed ceiling since it’s tied to your existing credit card limit. Spending limits on all apps increase over time as you build a repayment history with the provider.

Which BNPL apps work at any store?

Zip, Affirm, Klarna, and Afterpay all offer virtual cards that work at any merchant accepting Visa or Mastercard, including in-store purchases. Zip’s virtual card is the most broadly applicable for one-off store visits. PayPal Pay Later works at any merchant that accepts PayPal checkout, which covers most major e-commerce platforms.

The Bottom Line

No single app among the other apps like Klarna is the best choice for everyone. Afterpay handles everyday retail spending cleanly. Affirm is the most transparent option for larger financed purchases. Perpay solves the approval problem for buyers with bad credit. And Splitit is the only app that genuinely adds no new debt to your balance sheet.

The BNPL market has matured past the simple “four payments, zero interest” pitch that launched most of these apps. Nearly every major provider now offers a spectrum of plans, and the differences that matter most, fees when you miss payments, actual interest rates on longer plans, and how each app reports to credit bureaus, are buried in the fine print that most users skip entirely.

One thing these apps share is the premise that flexible payments make large purchases feel smaller. They do. But the buy now, pay later model also makes it easier to take on more debt across more vendors than a single credit card statement would ever reveal.